It is important to understand the basics of mortgages before you apply. This includes the interest rate, downpayment, assessment by the lender, and your personal information. Choosing the right mortgage to finance your home purchase is an important step. It can make a big difference in your life and your finances.

Interest rate

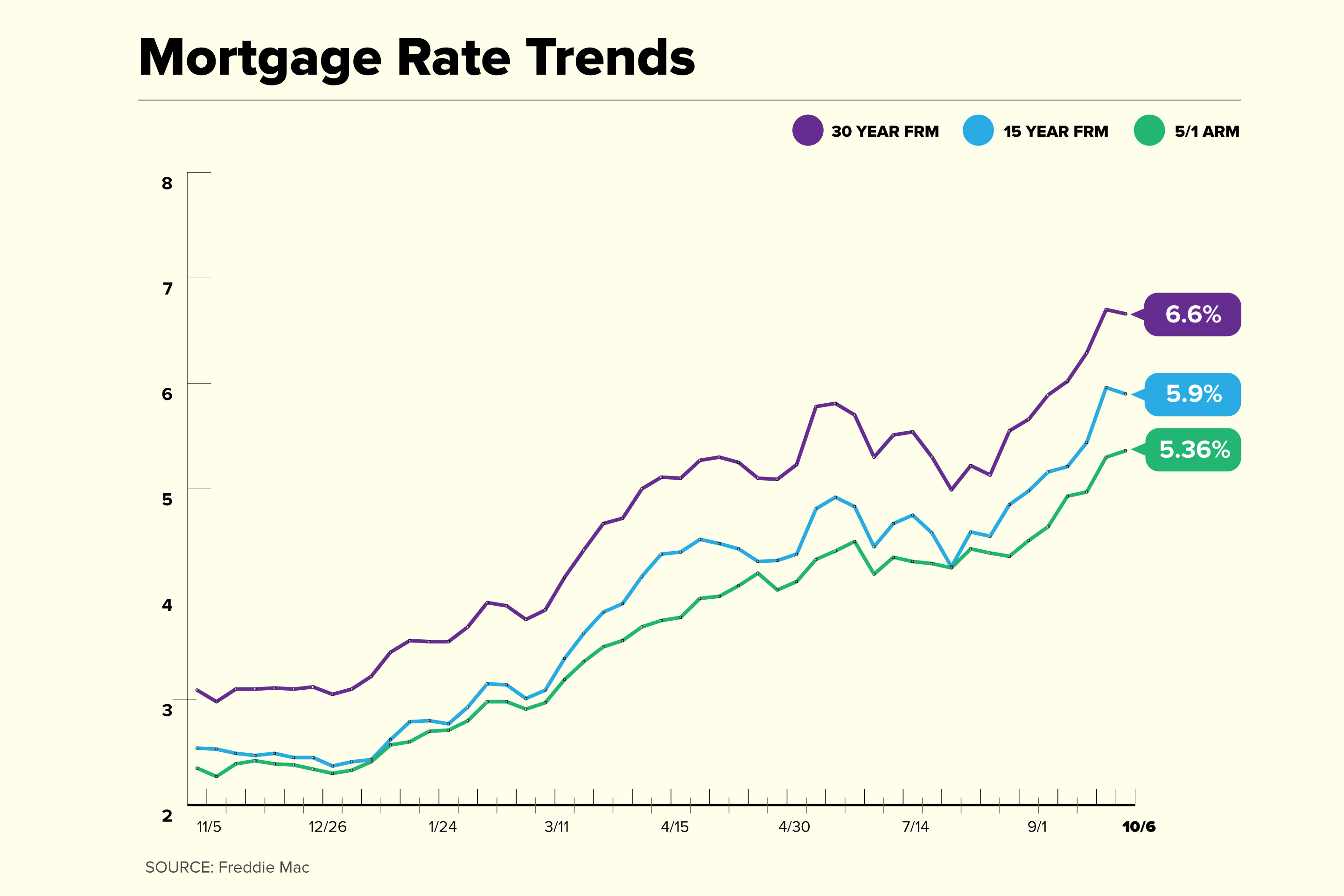

A percentage of the loan amount is used to calculate the interest rate for a mortgage. The interest rate is paid by the borrower in addition to the agreed loan repayments. Choosing the right mortgage interest rate is crucial for a person to be able to make their monthly payments. The mortgage interest rate can go up or down, so it is crucial to be on the lookout for changes.

Other costs related to the mortgage, such loan origination fees and discounts points, are not included in an interest rate. Mortgage insurance and closing costs are also included. The APR provides borrowers with a clear view of the total cost for borrowing.

Deposit payment

The down payment for a mortgage is a proportion of the home's total value that the borrower must pay up front. It usually ranges from ten to fifty percent. The interest rate that will be charged to a mortgage borrower will depend on the amount of their down payment. Generally, the larger the down payment, the lower the interest rate will be. A large downpayment decreases the risk in mortgage lending.

There are no hard and quick rules about how much down you should pay, but there are some things you can consider when you are deciding on your down payment. A low down payment can be risky so aim for at least 50 percent. A bank is more likely lend money to borrowers who are able put up fifty to sixty per cent of the purchase price. However, if your down payment is small or you don't have any savings, a bank will likely refuse to lend you money if you can't pay the full amount in a lump sum.

Lender's assessment of your information

A mortgage lender examines many factors to determine if your risk level. They will examine your credit history and any recent debt applications. These details may be verified by your employer. They will also examine your payment history and check to see if your payments have been paid on time. They'll also look at any assets that are substantial if you have them.

Lenders are interested in knowing if you can repay the loan. They may also look at your creditworthiness and your ability to handle more debt. To determine this, they check the five C's of credit: character, capacity, capital, collateral, and conditions.

Different types of mortgages

There are many types of mortgages. The conventional mortgage is the first type. A conventional mortgage can be used for most types of property. These loans are generally easier to qualify because they are backed by government. These mortgages are generally more appealing for first-time buyers, people with lower credit scores or higher debt-to income ratios.

The adjustable rate mortgage (ARM), is the second type. People who want to adjust their interest rates can choose adjustable-rate mortgages. Another type of government-backed loan would be an FHA, VA, USDA or USDA mortgage.

Refinancing options

There are many options for refinancing your mortgage. It is important to shop around for the best deal. Before you refinance, it is important to get quotes from multiple lenders. To help you navigate the complex paperwork, an attorney is also available.

Refinancing allows you to take advantage of the equity in your home. Refinancing will lower your monthly cost and make it possible to achieve your financial goals. Refinance your mortgage for a variety of reasons.

FAQ

What are the most important aspects of buying a house?

Location, price and size are the three most important aspects to consider when purchasing any type of home. Location refers to where you want to live. Price is the price you're willing pay for the property. Size is the amount of space you require.

How can I fix my roof

Roofs can become leaky due to wear and tear, weather conditions, or improper maintenance. Roofing contractors can help with minor repairs and replacements. Contact us for further information.

Can I buy a house without having a down payment?

Yes! Yes. There are programs that will allow those with small cash reserves to purchase a home. These programs include conventional mortgages, VA loans, USDA loans and government-backed loans (FHA), VA loan, USDA loans, as well as conventional loans. You can find more information on our website.

What should I be looking for in a mortgage agent?

A mortgage broker assists people who aren’t eligible for traditional mortgages. They work with a variety of lenders to find the best deal. Some brokers charge fees for this service. Others offer no cost services.

Do I need flood insurance

Flood Insurance covers flooding-related damages. Flood insurance protects your possessions and your mortgage payments. Learn more about flood coverage here.

How much money do I need to save before buying a home?

It depends on how much time you intend to stay there. It is important to start saving as soon as you can if you intend to stay there for more than five years. If you plan to move in two years, you don't need to worry as much.

What amount of money can I get for my house?

It depends on many factors such as the condition of the home and how long it has been on the marketplace. Zillow.com reports that the average selling price of a US home is $203,000. This

Statistics

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

External Links

How To

How to Find Real Estate Agents

The real estate agent plays a crucial role in the market. They are responsible for selling homes and property, providing property management services and legal advice. Experience in the field, knowledge about your area and great communication skills are all necessary for a top-rated real estate agent. You can look online for reviews and ask your friends and family to recommend qualified professionals. You may also want to consider hiring a local realtor who specializes in your specific needs.

Realtors work with buyers and sellers of residential properties. A realtor helps clients to buy or sell their homes. A realtor helps clients find the right house. They also help with negotiations, inspections, and coordination of closing costs. A majority of realtors charge a commission fee depending on the property's sale price. Unless the transaction is completed, however some realtors may not charge any fees.

The National Association of Realtors(r) (NAR), offers many different types of real estate agents. To become a member of NAR, licensed realtors must pass a test. Certification is a requirement for all realtors. They must take a course, pass an exam and complete the required paperwork. NAR recognizes professionals as accredited realtors who have met certain standards.