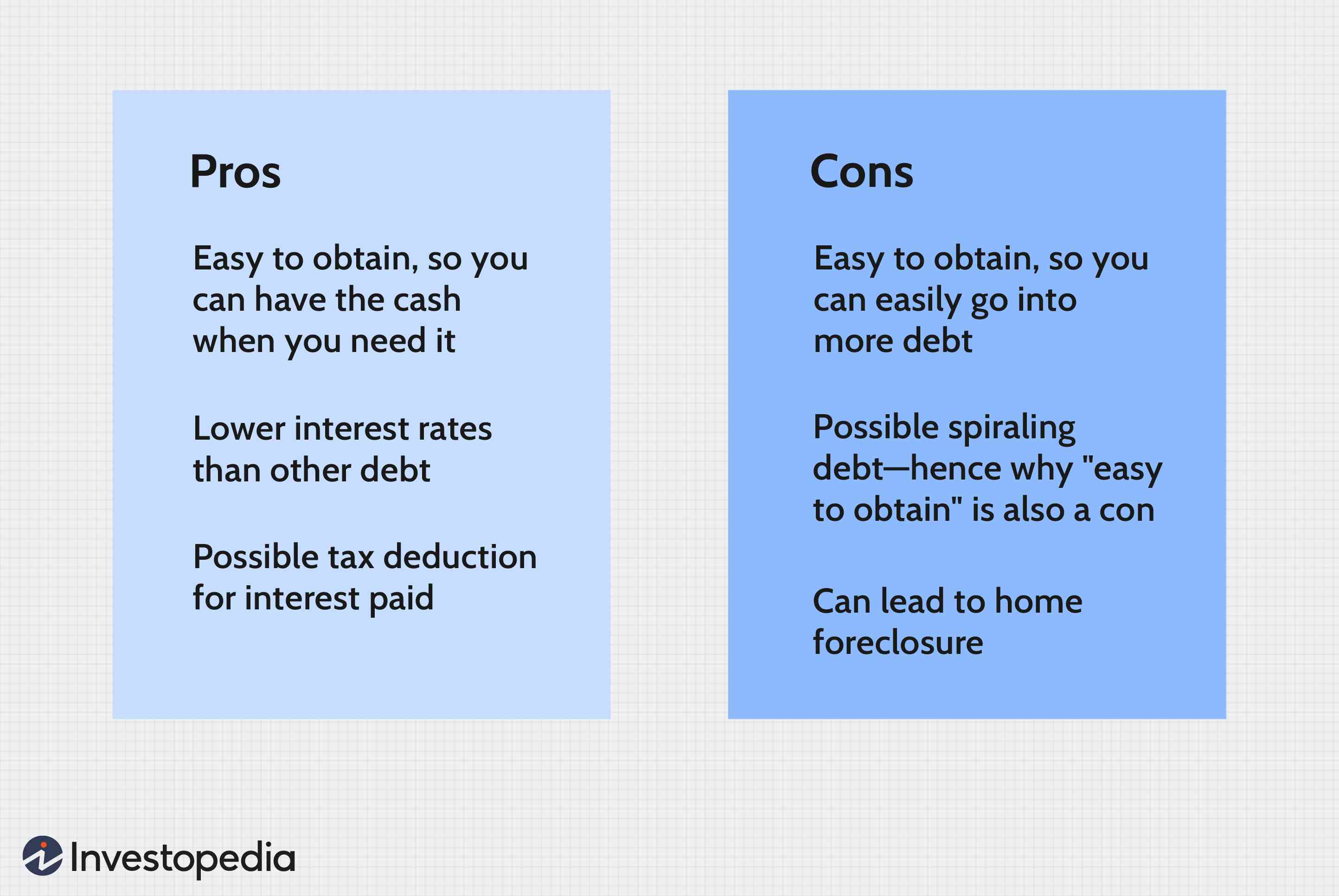

Personal loans can be more advantageous than home equity loan when it comes to borrowing money for home improvements or debt consolidation. However, home equity loans can offer tax advantages and a shorter repayment period. If you're new to home ownership, you may not have enough equity in your home. Equity is your home's total value less the amount you owe. This equity can take many years to build depending on how quickly you pay your mortgage off and how high your home's value increases.

Repayment terms for personal loans are shorter

Personal loans typically have repayment terms between two and seven year, but some lenders may offer longer terms. In general, a personal loan's shorter repayment term means a lower total interest charge over the term of the loan. Personal loans have higher interest rates that home equity loans, but they tend to be more expensive. Personal loans may also have a lower minimum loan amount.

A personal loan is typically easier to qualify for than a home-equity loan. The application process should be quick and easy. However, if you have a poor credit score, you may be charged a higher interest rate than someone with excellent credit. This could put you in a more risky position, and even lead to your losing your home.

A personal loan also has the benefit of flexibility. Personal loans generally have shorter repayment terms than home equity loans. Personal loans are often used for a variety of reasons, including paying off credit card debts and paying for a home improvement project. Lenders also assess your credit rating and ability to repay the loan. You should be able to qualify for a personal loan if your credit score is good.

Higher interest rates

Consider the interest rate before deciding between a loan for home equity and a personal loan. While personal loans usually have a lower interest rate that home equity loans, their terms can often be longer. Home equity loans are secured by the property, so you risk losing your home if the payments are not made on time.

Personal loans typically have a term of between two and seven years. However, some lenders may offer loans with longer terms. The term for a home equity loan is five to thirty years. You will need to repay the loan using the proceeds from the sale of your house.

The interest rate for a home equity loan is usually between 5%-6%. Although the interest rate for a home equity loan can fluctuate over time it is still much lower than a personal loan. Additionally, the interest rate for a home-equity loan will be determined by your credit score and income. Personal loans won't have fixed interest rates.

Repayment terms that are longer

Home equity loans and personal loan both have advantages and disadvantages in borrowing money. Personal loans are not collateral-free and have lower interest rates. However, they do require borrowers to have good credit. Personal loans can often be funded faster.

If you have a strong credit history, but no equity in your home, personal loans may be a better option. They can also be more costly and may have higher fees if you are late paying or your fault. Personal loans can sometimes create more debt than home equity loans in some cases, particularly if they are used to repay credit cards.

For those who need more money, home equity loans can be a better option. These loans usually have lower interest rates and longer repayment terms which can help borrowers pay down their debts quicker. In addition, they may be more affordable for those who have substantial equity in their home. Both types are suitable for debt consolidation, emergency funds, and educational costs.

FAQ

Should I rent or buy a condominium?

Renting might be an option if your condo is only for a brief period. Renting will allow you to avoid the monthly maintenance fees and other charges. However, purchasing a condo grants you ownership rights to the unit. You can use the space as you see fit.

Should I use a broker to help me with my mortgage?

Consider a mortgage broker if you want to get a better rate. Brokers are able to work with multiple lenders and help you negotiate the best rate. Some brokers receive a commission from lenders. Before signing up, you should verify all fees associated with the broker.

How much money do I need to purchase my home?

This varies greatly based on several factors, such as the condition of your home and the amount of time it has been on the market. Zillow.com says that the average selling cost for a US house is $203,000 This

What are the top three factors in buying a home?

The three most important things when buying any kind of home are size, price, or location. Location is the location you choose to live. The price refers to the amount you are willing to pay for the property. Size refers the area you need.

How much should I save before I buy a home?

It depends on how much time you intend to stay there. Save now if the goal is to stay for at most five years. But, if your goal is to move within the next two-years, you don’t have to be too concerned.

How can I get rid Termites & Other Pests?

Termites and many other pests can cause serious damage to your home. They can cause serious destruction to wooden structures like decks and furniture. You can prevent this by hiring a professional pest control company that will inspect your home on a regular basis.

Statistics

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

External Links

How To

How do I find an apartment?

Moving to a new place is only the beginning. This involves planning and research. This includes researching the neighborhood, reviewing reviews, and making phone call. You have many options. Some are more difficult than others. Before renting an apartment, it is important to consider the following.

-

Researching neighborhoods involves gathering data online and offline. Online resources include Yelp. Zillow. Trulia. Realtor.com. Local newspapers, landlords or friends of neighbors are some other offline sources.

-

Find out what other people think about the area. Review sites like Yelp, TripAdvisor, and Amazon have detailed reviews of apartments and houses. You can also find local newspapers and visit your local library.

-

To get more information on the area, call people who have lived in it. Ask them what they loved and disliked about the area. Ask if they have any suggestions for great places to live.

-

You should consider the rent costs in the area you are interested. Consider renting somewhere that is less expensive if food is your main concern. Consider moving to a higher-end location if you expect to spend a lot money on entertainment.

-

Learn more about the apartment community you are interested in. Is it large? What is the cost of it? Is it pet-friendly? What amenities does it offer? Do you need parking, or can you park nearby? Do you have any special rules applicable to tenants?