A home mortgage calculator is an automated tool that helps homeowners calculate the monetary impacts of various variables. It is simple to use and can help homeowners save time and money. In addition, a home refinance calculator can help homeowners make the right financial decisions for their individual needs. A home refinance calculator is easy to use. Simply enter some basic information and you will be able to find the best rate for both your home, and your budget.

Tax-free cash out refinance

You can make great home improvements with the cash you receive from a cash out home refinance. A cash-out refinance will not be free of cost. You will have to pay interest. It is debt. However, the Tax Cuts and Jobs Act of 2018 will not require you to report the money income.

Refinances of homes with cash are exempt from taxes because the money is not treated as income. The IRS considers equity received from a home-refinance cash-out as an additional loan rather than income. However, it's important to understand that cash-out home refinances have different rules than traditional mortgages. There are guidelines regarding the maximum amount of mortgage points you can deduct.

Refinance to a loan with a longer term

Refinancing is a great option to reduce your monthly payments as well as take advantage lower interest rates. It may also allow you to pay off your mortgage faster and build equity sooner. Refinancing your home comes with its own risks and disadvantages. Our mortgage calculator can help you estimate your monthly cost.

Refinancing your home is an option. Make sure you consider the loan term. A shorter term will help you save thousands of dollars over the life of your loan.

Tax benefits of refinancing

You might be curious if refinancing your home will give you any tax benefits. The truth is that refinancing costs aren't tax deductible, but the lender's appraisal of your home's worth might be. It could be because of escalating property values or because your lender's appraisal was greater than the tax authority's.

However, refinancing offers its fair share tax benefits. One of these benefits is the ability to deduct mortgage points. Points, which are equal to 1% of the loan balance, are deductible over the life of the loan. This deduction is available if you refinance your primary property or another qualifying property. If you refinance to receive a lower rate of interest, you can also subtract your discount points.

Common fees involved in refinancing

When pursuing a home refinancing loan, applicants should be aware of the common fees involved. Most lenders charge an application fees, which can vary from $75 to 300. The fee covers administrative costs, such as evaluating loan eligibility. Some lenders also charge a loan origination fee of 0.5% to 1.5% of the loan amount. Additional fees may be charged by lenders for title searches, which can range from $200 to $400.

A loan that has a higher interest rate will usually be more expensive than one which has a lower. The loan balance can be used to finance fees if you have sufficient equity in your home. Alternatively, you can cash out some of the money you saved in the process. Refinances should be discussed with your lender to determine if there are any savings.

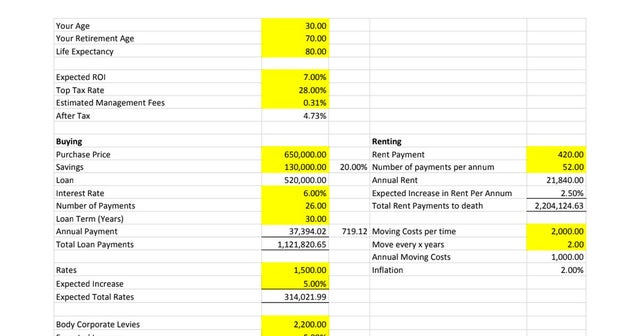

Using the calculator

You can use a home finance calculator to determine how much money you can afford for your home. You can use this calculator to determine your monthly payments and the amount you need for down payments. The calculator can also calculate monthly homeowners insurance and property taxes. In many cases, the calculator will calculate these costs automatically for you, making the process as easy as possible for you.

This calculator can help you calculate your monthly payment by calculating your down payment and interest rate. You can enter a specified amount or a range. If you are looking to buy a $150,000 home the calculator will calculate your monthly payment. You can now compare the various mortgage rates and options once you know your monthly payments.

FAQ

What should I do before I purchase a house in my area?

It all depends on how many years you plan to remain there. It is important to start saving as soon as you can if you intend to stay there for more than five years. If you plan to move in two years, you don't need to worry as much.

How long does it usually take to get your mortgage approved?

It all depends on your credit score, income level, and type of loan. It usually takes between 30 and 60 days to get approved for a mortgage.

What should I look out for in a mortgage broker

A mortgage broker is someone who helps people who are not eligible for traditional loans. They shop around for the best deal and compare rates from various lenders. Some brokers charge fees for this service. Some brokers offer services for free.

Is it possible to sell a house fast?

You may be able to sell your house quickly if you intend to move out of the current residence in the next few weeks. But there are some important things you need to know before selling your house. First, you must find a buyer and make a contract. You must prepare your home for sale. Third, it is important to market your property. You should also be open to accepting offers.

What are the drawbacks of a fixed rate mortgage?

Fixed-rate loans are more expensive than adjustable-rate mortgages because they have higher initial costs. Also, if you decide to sell your home before the end of the term, you may face a steep loss due to the difference between the sale price and the outstanding balance.

What are the pros and cons of a fixed-rate loan?

With a fixed-rate mortgage, you lock in the interest rate for the life of the loan. This will ensure that there are no rising interest rates. Fixed-rate loan payments have lower interest rates because they are fixed for a certain term.

Can I buy a house without having a down payment?

Yes! There are many programs that can help people who don’t have a lot of money to purchase a property. These programs include conventional mortgages, VA loans, USDA loans and government-backed loans (FHA), VA loan, USDA loans, as well as conventional loans. More information is available on our website.

Statistics

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

External Links

How To

How to Rent a House

Finding houses to rent is one of the most common tasks for people who want to move into new places. But finding the right house can take some time. When it comes to choosing a property, there are many factors you should consider. These include location, size, number of rooms, amenities, price range, etc.

It is important to start searching for properties early in order to get the best deal. Ask your family and friends for recommendations. This way, you'll have plenty of options to choose from.