You can use a calculator to determine whether you are able to afford a home. This calculator will allow you to input various factors like your down payment, interest rate, property taxes, and more. The results will depend on your credit score as well as other factors. These results may differ depending on market conditions, your mortgage selection, lender guidelines, or your mortgage selection. Keep in mind that these results may be rounded up or down and may not be accurate.

Deposit payment

A down payment on an affordable loan calculator is a helpful tool when determining the amount of down payment you can afford. The calculator will estimate the price for a home based upon your gross monthly salary, down payment and debt. The down payment amount is one of the most important factors that determine affordability.

A down payment calculator comes in handy if you're not sure what your budget is or how much money to put down. The calculator will calculate your down payment based on the cost of the home you want to purchase. You can adjust your homeowners insurance rate and amount, which will likely be included in the mortgage payment.

Your credit score is a critical aspect of your finances. It will determine your mortgage rate. A credit score greater than 740 will allow you to get the best rate and most affordable monthly payment for your mortgage loan. A low credit score may result in monthly mortgage payments of $300. One of these agencies can help you check your credit score.

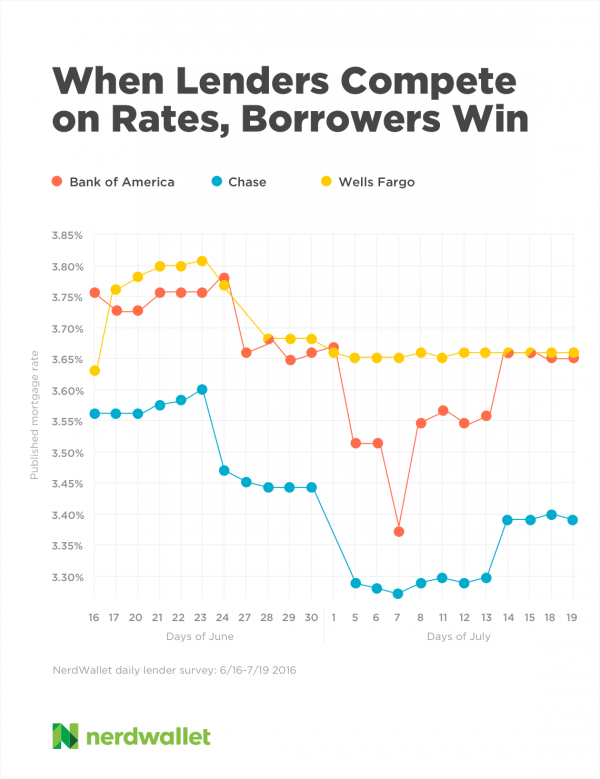

Interest rate

Consider the interest rate before you apply for a loan. Interest rates are a percentage on the total loan amount. To calculate your interest rate, the affordability calculator uses a national average mortgage rate. However, your actual rate will depend on other factors such as your down payment.

Once you know the interest rate, the next step is to determine how much your monthly payment will be. The affordability calculator will calculate the total payment. This includes the interest rate, homeowner's insurance, and property taxes. Once you have an idea of your financial capabilities, you can determine what home prices you can afford.

Property taxes

If you're buying a house, you'll need to figure out how much property taxes will cost. The cost of property taxes will depend on where you live and how much your home is worth. For an estimate of what you will have to pay, you can either do research online or talk to a professional. Most homeowners pay their taxes through an escrow account that's attached to their mortgage payments. For example, a $100,000 home would cost $1,000 a year in property taxes.

You can find the average tax rate for your local area with a property tax calculator. These rates can vary greatly between states and counties. For example, property taxes can increase the cost of a New Jersey house by more than one per cent, while Wyoming homes will have a lower cost.

FAQ

How do I calculate my interest rates?

Interest rates change daily based on market conditions. In the last week, the average interest rate was 4.39%. The interest rate is calculated by multiplying the amount of time you are financing with the interest rate. Example: You finance $200,000 in 20 years, at 5% per month, and your interest rate is 0.05 x 20.1%. This equals ten bases points.

What are the advantages of a fixed rate mortgage?

Fixed-rate mortgages allow you to lock in the interest rate throughout the loan's term. This guarantees that your interest rate will not rise. Fixed-rate loans also come with lower payments because they're locked in for a set term.

Should I buy or rent a condo in the city?

Renting could be a good choice if you intend to rent your condo for a shorter period. Renting lets you save on maintenance fees as well as other monthly fees. However, purchasing a condo grants you ownership rights to the unit. The space is yours to use as you please.

Is it better buy or rent?

Renting is typically cheaper than buying your home. But, it's important to understand that you'll have to pay for additional expenses like utilities, repairs, and maintenance. The benefits of buying a house are not only obvious but also numerous. You will be able to have greater control over your life.

Statistics

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

External Links

How To

How to Find Houses To Rent

For people looking to move, finding houses to rent is a common task. Finding the perfect house can take time. When you are looking for a home, many factors will affect your decision-making process. These factors include location, size and number of rooms as well as amenities and price range.

To make sure you get the best possible deal, we recommend that you start looking for properties early. For recommendations, you can also ask family members, landlords and real estate agents as well as property managers. This will allow you to have many choices.