A down payment will reduce the amount the lender has to lend you in order to purchase your home. A 20% down payment, for example, will lower the amount of money the lender has to worry about getting back if you stop paying. It is important to note that the down payment requirement is not set by the lender alone. It is also set and determined by the investor, who will be financing the loan.

For down payment, save

An important step towards buying a home is to save money for a downpayment. It is similar to running marathons: you need to save one dollar each day while making sure your finances are in order. It is possible to set up a budget to save money for a down payment.

Re-selling your items at home is one way to save some money on your down payment. This can be done through online marketplaces, local pawn shops and consignment stores. You can also sell your items at a yard sales to raise money for your downpayment. Also, include your partner’s income.

Documentation required

You will need the appropriate documentation in order to obtain a mortgage. Your down payment funds will need to be verified by the lender. Even if you are sending a check from overseas, the lender will need to verify where the funds came from. Lenders typically require a downpayment to close the loan. But there are exceptions.

Most mortgage lenders require you to show them your tax returns for the last two years. The most recent federal and state tax returns are typically required. They might also require additional income documentation.

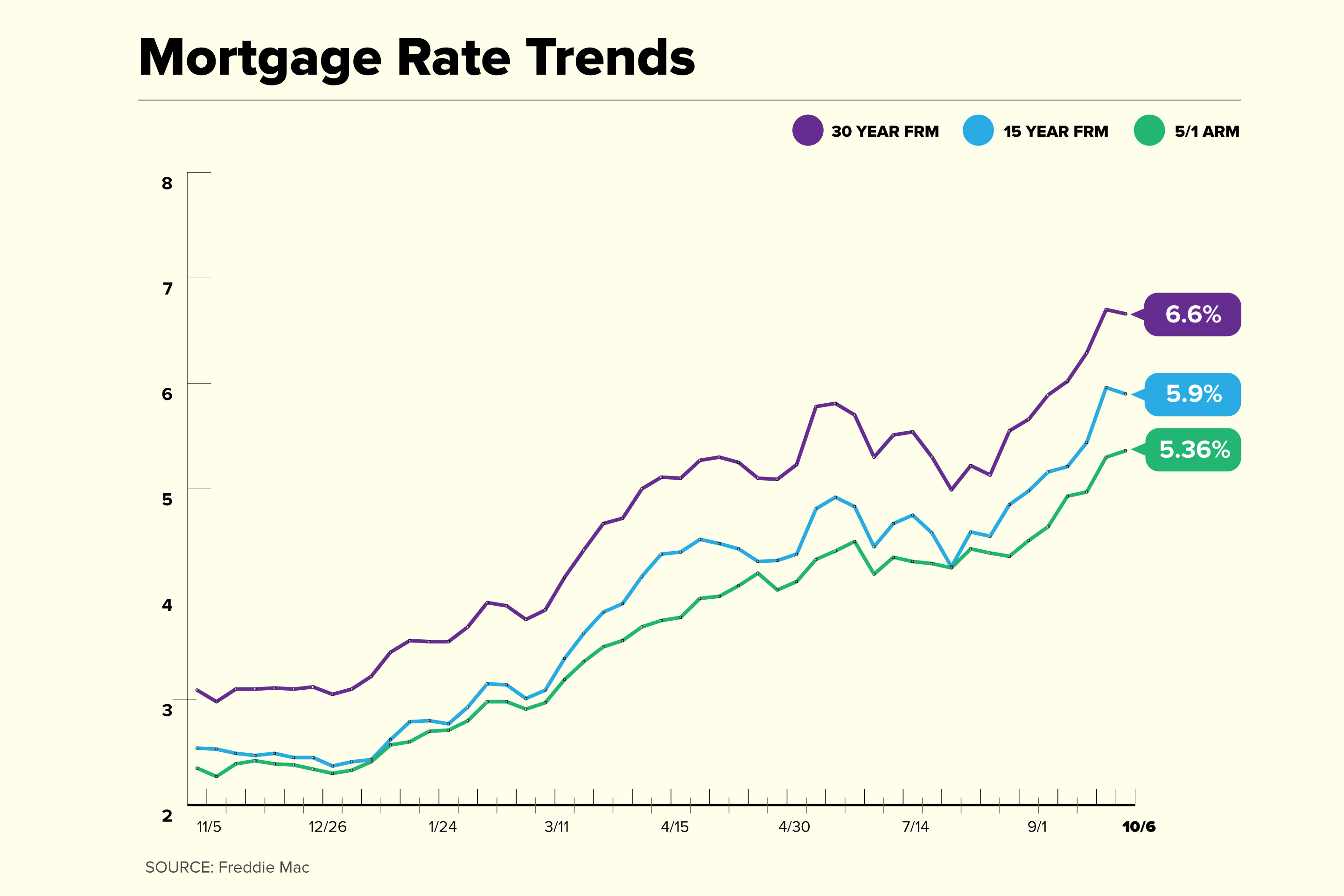

Average down payment

This year has seen historic mortgage rates fall to record lows. This is fueling a vibrant housing market. But what is an average downpayment? It depends on your state of residence. The average downpayment required to get a mortgage in California was more than $100k as of June 20, 2021. Only a few other states had lower down payments, with the median being less than $10k. The larger your down payment, you'll have more equity in your home.

Many people will choose to put down less than 20%, even though some lenders require that you pay 20%. A lower down payment will allow you to reach your goal faster. Consider all pros and cons when deciding on the amount of your down payment.

Save on PMI

PMI is a way to save money on your mortgage but it comes with a cost. PMI costs can range from 0.3 to 1.5% of your loan amount. This extra fee may be paid at closing or added to your monthly payment. These costs vary with different mortgages.

One way to save on PMI is to pay for it upfront. While this reduces your monthly payments, it may mean a higher annual cost that may not be refundable in the event you move. Another option is to make partial payments each month and save on monthly premiums. This is especially useful if you are trying to save money early in the year, or if you don't have much down payment.

Impact of down payment on loan-to–value ratio

The down payment on mortgages has a big impact on the loan–to-value ratio (LTV). A larger down payment will lead to a lower LTV ratio. This is because your equity will be greater if you have a lower LTV. To make your mortgage smaller, increase your downpayment if it is low.

A loan with an 80% LTV can be obtained if the down payment is 10% of total price. This will lower your chance of default and reduce your monthly payments. Bankrate has a mortgage calculator you can use to calculate how much you will have to deposit on your mortgage.

FAQ

What are the pros and cons of a fixed-rate loan?

Fixed-rate mortgages lock you in to the same interest rate for the entire term of your loan. This ensures that you don't have to worry if interest rates rise. Fixed-rate loans come with lower payments as they are locked in for a specified term.

How do I fix my roof

Roofs can leak due to age, wear, improper maintenance, or weather issues. For minor repairs and replacements, roofing contractors are available. Contact us for further information.

What is reverse mortgage?

A reverse mortgage allows you to borrow money from your house without having to sell any of the equity. It allows you to borrow money from your home while still living in it. There are two types available: FHA (government-insured) and conventional. A conventional reverse mortgage requires that you repay the entire amount borrowed, plus an origination fee. If you choose FHA insurance, the repayment is covered by the federal government.

How much does it cost to replace windows?

Replacing windows costs between $1,500-$3,000 per window. The total cost of replacing all of your windows will depend on the exact size, style, and brand of windows you choose.

How much money will I get for my home?

This can vary greatly depending on many factors like the condition of your house and how long it's been on the market. Zillow.com says that the average selling cost for a US house is $203,000 This

Statistics

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

External Links

How To

How to Purchase a Mobile Home

Mobile homes are houses built on wheels and towed behind one or more vehicles. Mobile homes have been around since World War II when soldiers who lost their homes in wartime used them. Today, mobile homes are also used by people who want to live out of town. These houses are available in many sizes. Some houses are small, others can accommodate multiple families. There are even some tiny ones designed just for pets!

There are two types main mobile homes. The first is made in factories, where workers build them one by one. This process takes place before delivery to the customer. Another option is to build your own mobile home yourself. Decide the size and features you require. Next, ensure you have all necessary materials to build the house. Final, you'll need permits to construct your new home.

These are the three main things you need to consider when buying a mobile-home. Because you won't always be able to access a garage, you might consider choosing a model with more space. You might also consider a larger living space if your intention is to move right away. Third, make sure to inspect the trailer. If any part of the frame is damaged, it could cause problems later.

Before buying a mobile home, you should know how much you can spend. It is important to compare prices across different models and manufacturers. It is important to inspect the condition of trailers. Although many dealerships offer financing options, interest rates will vary depending on the lender.

It is possible to rent a mobile house instead of buying one. Renting allows you to test drive a particular model without making a commitment. Renting is expensive. Renters generally pay $300 per calendar month.